Insurance

RBNZ clearly has life insurance commission in its sights

Wednesday 28th of November 2018

It released its latest Financial Stability report this week, which looks at the banking and insurance sectors.

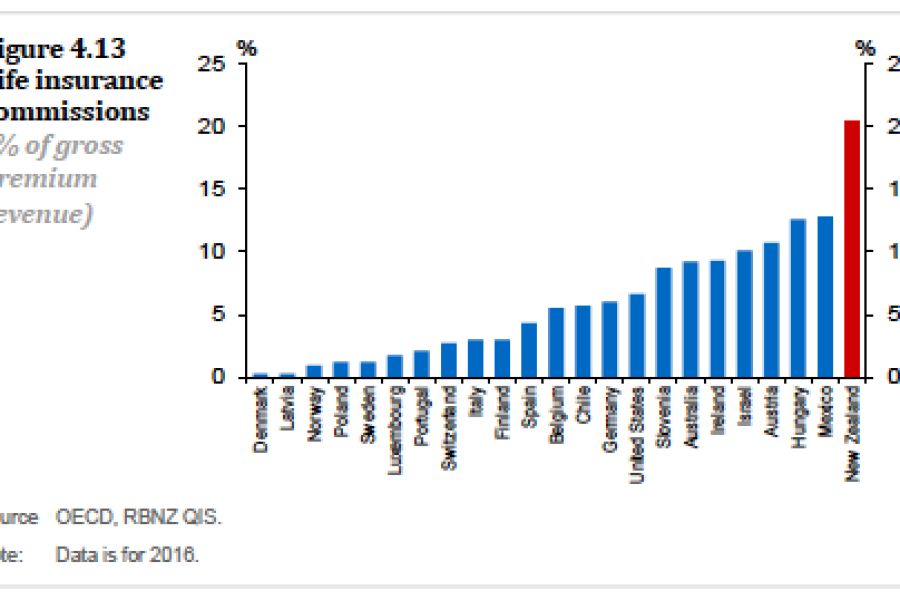

The report highlighted life insurers' tendency to rely on financial advisers, rather than shifting to online and direct distribution as many general insurance providers have done.

It compared commission in New Zealand to that paid by insurers in other countries and...

Want to read the full article?

Click the button below to subscribe and will have unlimited access to full article and all other articles on the site.

Latest News